In 2019, a single piece of legislation known as the Small Electric Vehicle Ordinance cleared the way for e-scooters in Germany. Since then, they have conquered the big cities and become an indispensable form of transport on roads and bike lanes. But from the beginning, this new form of mobility has been highly controversial: while many urban citizens and commuters find e-scooters extremely practical for getting around, others feel harassed or even threatened by electric scooters zipping around the place.

Importantly, the legislation excludes e-scooters from the same strict liability, like slow-moving motor vehicles such as motorised wheelchairs and certain agricultural machinery with a maximum speed of up to 20 km/h. However, over the past couple of years, the number of accidents and damages caused by e-scooters, has caused many traffic experts to question the extent to which this privileged treatment is appropriate in terms of liability. For example, in 2021, more than 2,011 incidents involving e-scooters injured 2,020 people, 386 of them seriously. Five people died. In almost every third accident, the driver was primarily responsible.

According to the German Insurance Association (GDV), pay-outs in claims for third-party liability involving e-scooters rose by 108.9% to around 8 million euros in 2021. Property damage accounted for 55.9% and personal injury for 44.1%. These figures must of course be weighed against the significant rise in the number of insured risks overall last year. But for comparison, the average claim for very small electric vehicles hardly changed – and at 3,247 euros it was significantly lower than the figure for passenger cars (4,676 euros).

Due to the rapid spread of e-scooters, especially in built-up, inner metropolitan areas, and the overall increase in traffic density, a further increase in accidents can be expected in the future. And the current exclusion of strict liability means injured parties are often not adequately protected. Without the existence of an operational risk, proof that the injuring party was at fault must be provided for any damage claim against them to be upheld.

Claims expenditure 2021 for e-scooter motor

(+109% compared to the previous year)

Source: German Insurance Association (GDV)

Legislators have not yet responded to the growing problem of accidents involving e-scooters. In the meantime, the German Council on Jurisdiction in Traffic has taken the initiative. In August, experts from a working group on liability law for slow-moving vehicles crafted a recommendation to the legislature to fundamentally reform liability. The general statutory exclusion of strict liability is no longer appropriate given the changed conditions in road traffic. Considering the high hazard potential of e-scooters – especially in light of increased usage and limitations on traffic space – they should be subject to stricter liability.

The big question is whether the federal government will take up the issue and adopt the legal changes the Council on Jurisdiction in Traffic are calling for. Insurers should be mindful of the high risk of policy change in e-scooter coverage and assess what risks exist today and what impact the introduction of strict liability could have on future calculations and expenditures.

Larissa Klick, Motor Product Manager at Deutsche Rück

The liability risks are manifold: in addition to the sometimes serious personal injuries caused by e-scooter accidents, the damage caused by parked scooters must also be considered. Pedestrians can be harmed if e-scooters are parked inappropriately or left on footpaths, as has been seen time and again. In addition, parked cars can also be damaged by scooters falling over. And there is a possible accumulation risk from e-scooter batteries: there have been expensive claims cases where a faulty self-igniting battery in a warehouse caused a fleet of scooters to go up in flames. Privately owned e-scooters also carry the risk of the batteries igniting and causing fire damage while charging at home.

So far, the attitude of insurers toward e-scooters has been as heterogeneous as the attitude of the general public. Part of the industry is actively engaged in covering the new risk and sees it as an entry-level product, especially for younger customers. The other part remains sceptical and doubts whether the effort is worthwhile for what is ultimately a rather small premium. Therefore, some insurers cover e-scooters in their product range only to “round them off”, so that they can offer customers coverage in case of doubt and not lose out to the competition.

The price differential is correspondingly wide: For drivers under the age of 23, for example, the range currently extends from 17 euros to around 90 euros in annual premiums. As this segment is all new, a sensible basis for calculation must obviously still be established. Larissa Klick also points out another special phenomenon that affects the liability risks of e-scooters: “Many younger people today have no motor vehicle experience at all because, especially in urban areas, a driver’s license is no longer part of growing up as it was in decades past. Accordingly, the accident risk of the mostly younger e-scooter riders must be assessed as higher.”

In any event, insurers that want to take advantage of the opportunities offered by e-scooter coverage and therefore tap into a growing market must be fully cognisant of the specific risks of this still emerging form of mobility.

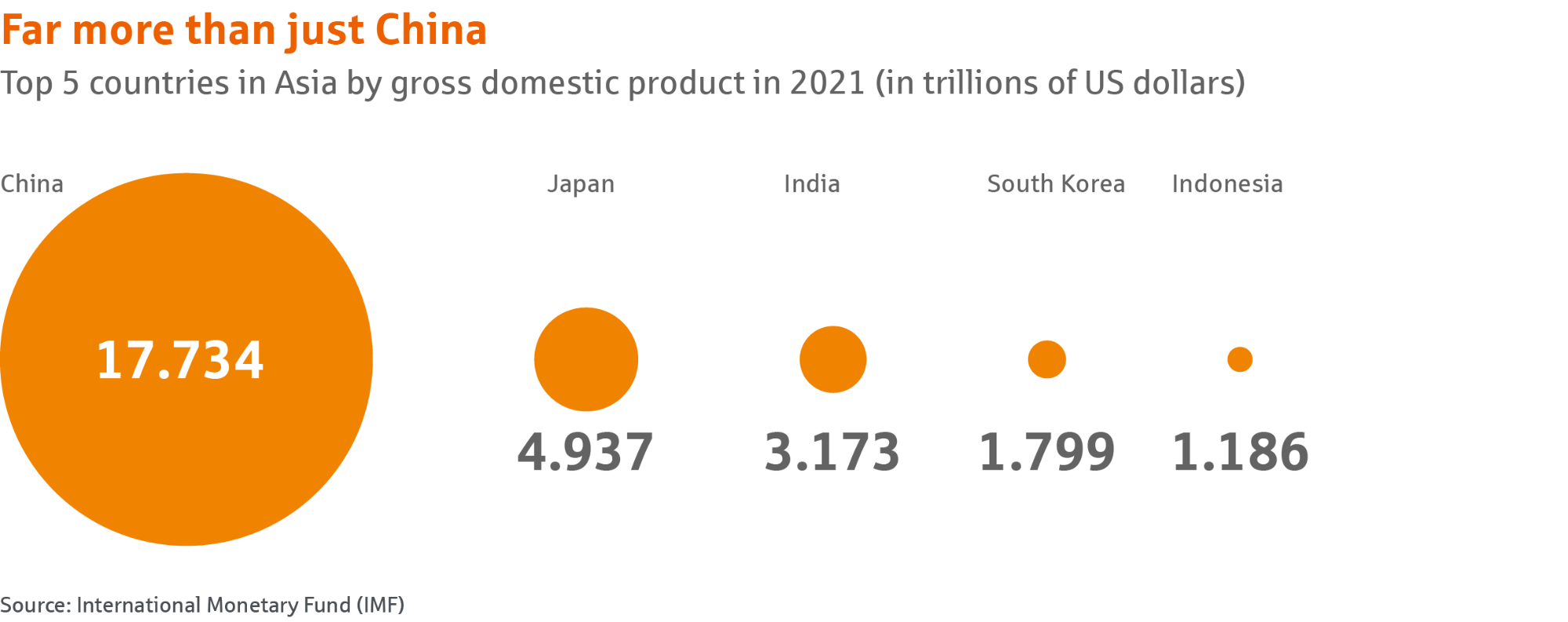

In the south and east of Asia, the economy is growing rapidly – and with it, the prosperity of the population. This makes the market interesting for insurers and reinsurers. Furthermore, many countries in the region are making a rapid recovery from the effects of the pandemic. Deutsche Rück is now also exploring its business prospects in Asia.

The speed at which the middle class is growing in countries in South, East and Southeast Asia is astonishing. According to the Brookings Institute, the number of people on the Asian continent who belong to the middle class will grow from about 2 billion in 2020 to 3.5 billion in 2030. According to the study, almost two-thirds of the global middle class will come from Asia in the future.

The background to this development is that many countries in South and East Asia have gained enormous economic muscle in recent years. Since 1995, for example, the Indian economy has grown steadily – by an average of more than six percent annually. And the Asian Development Bank (ADB) expects the economic performance of the emerging markets in Asia to continue to grow robustly in the coming year. One of the knock-on effects is that many countries are even leaving China – once the global dynamo of growth – behind. Expansion in the People’s Republic has cooled in recent years, partly due to the country’s lockdown policy. However, many other emerging markets in Asia appear to be overcoming problems associated with the pandemic more quickly. While not immune to the effects of inflation and the war in Ukraine, they are fast catching up. “Economic recovery is underway in most countries in East Asia and the Pacific,” says Manuela Ferro, World Bank Vice President for East Asia and the Pacific.

The result of this development is that while the Chinese economy will grow by only 3.3 percent in 2022, according to ADB figures, all other emerging Asian economies will grow by an average of 5.3 percent. By comparison, Germany will see growth of just 1.4 percent in 2022, according to a forecast by the federal government.

The dynamic economic environment in many Asian countries also makes the market there interesting for the insurance industry. Deutsche Rück, for example, will start writing business for the first time in several countries in South, Southeast and East Asia, starting with selected markets in January 2023. Tarik Aouad, managing director for the Middle East/Asia department of Deutsche Rück, is leading the market entry in the region. He has more than two decades of experience in various reinsurance positions and has led the Middle East market segment at Deutsche Rück since 2020.

Aouad’s goal is to establish lasting business relationships with small and medium-sized local and regional primary insurers. “First, it’s about building mutual trust,” Aouad says. In doing so, his team will concentrate on Standard Property & Casualty business with a focus on appropriate profitability.

In terms of economic growth, India, Asia’s third-largest economy after China and Japan, is far ahead. Although the consequences of the Ukraine war and rising oil prices are weighing on the subcontinent’s economic development, the ADB forecasts economic growth there of around seven percent in both 2022 and 2023. India’s service sector, which includes hotels, transportation, IT and insurance, is considered one of the country’s growth engines. This also creates good business opportunities for insurers on the subcontinent. According to the Insurance Regulatory and Development Authority of India (IRDAI), insurance penetration (premiums of primary insurers as a percentage of national GDP) for non-life insurance products in India was just one percent in 2020-2021 – significantly below the global average of 3.9 percent.

Alongside India, the South Asian country of Bangladesh, with a population of more than 165 million, is one of the trailblazers in South Asia. The country came through the pandemic economically well and, according to the International Monetary Fund (IMF), already achieved growth of almost seven percent last year.

Other countries in Asia are also recovering in leaps and bounds from the past two years or corona-related disruption. According to IMF forecasts, Vietnam’s economy will grow by seven percent in 2022 – one of the reasons why it is likely to see rising foreign investment.

Malaysia is also on an upward trajectory – the growth forecast for 2022 is more than five percent. This positive development is based, among other things, on rising domestic consumption. Malaysia is a strong exporting nation – its most important industry is semiconductors, which are in constant global demand. In addition to manufacturing, the service sector is also doing very well. Taiwan’s economy weathered the corona pandemic well and did not shrink. Exports are the country’s driving economic force: its main products destined for foreign markets are electronic components and IT equipment, which accounted for more than half of all exports in 2021. The country has experienced booming annual growth over the past two years: 3.4 percent in 2020 and 6.6 percent in 2021. Forecasts for growth in the current year are around 3.3 percent.

Tarik Aouad is pleased to report that Deutsche Rück is building a reputation as a reliable reinsurer amongst many potential clients in Asia. The company has already received initial positive feedback and has good chances of establishing itself in Asia due to strong economic growth, he says. Aouad estimates the pace of market entry will not be the same in all countries and with all business partners. “This will depend on the respective market opportunities.” In entering the market, Deutsche Rück relies on both its existing network and cooperation with local brokers, Aouad says. “Our focus is on building long-term, mutually profitable customer relationships.”

At the top of the list of business risks that threaten a company’s existence is business interruption. One in five interruptions to “business-as-usual” is due to damage caused by fire. Using artificial intelligence (AI)-assisted video technology, companies today can protect themselves from fire on an ongoing basis to avoid disruption. The new generation of smart thermal cameras significantly contributes to loss prevention. The advantage for primary insurers is clear: they can now actively evaluate the use of the technology and create premium incentives.

Infrared thermography is already established as an inspection method in industrial plants – a manual procedure that only trained personnel or external experts are allowed to perform. Inspections with infrared cameras take place at set intervals. Through this process, defects in electrical systems can be detected at an early stage, thermally stressed components can be accurately located and damage can therefore be prevented. The advantage of this good practice is that ongoing operations do not have to be paused. However, intermittent manual inspections do not provide a perfect overview – faults that occur between inspections may remain undetected.

Many companies are now using their own thermal cameras to monitor their production facilities continuously and automatically, thereby significantly reducing their exposure to risk and improving fire protection. Like infrared thermography, automated thermal detection systems locate areas of increased temperature at an early stage – the application ranges from detection of hot surfaces to detection of embers.

Thermal cameras are particularly useful where large, obscured or difficult-to-access areas need to be monitored. They provide a reliable overview of outdoor areas and warehouses and thorough monitoring of indoor areas, as well as power-sensitive areas such as production facilities or server rooms. In the meantime, VdS Schadenverhütung GmbH (VdS) has recognised and certified the first thermal video systems. This is an important step for primary insurers who can now actively evaluate the use of technology. Specifically, they can create incentives through premium discounts.

As well as fire protection, constant monitoring of production areas with thermal detectors opens up the potential for identifying other damage triggers.

For example, the technology can detect wear and tear on electrical components in good time, which enables operators to plan predictable maintenance work, implement it in a way that is compatible with production and thus prevent further damage or even a sudden shutdown.

Furthermore, by continuously measuring the ambient temperature, the technology can even reliably detect a sudden cold source, which may be due, for example, to a leak in a water or gas line. Locating these kinds of breaches at an early stage makes it possible to intervene immediately, preventing the damage from spreading unnoticed and can significantly limit the impact. In the best-case scenario, this reduces production stoppages and operational downtime.

Another area of application is burglary protection. For example, thermal cameras can detect non-authorised persons entering a facility when it is closed. Depending on the reporting line, they trigger the intrusion alarm system immediately or send a message to the technical control centre. And the systems can learn and adapt. With the help of so-called “deep learning”, an important component of AI, false alarms are prevented and target searches are faster. This is because the thermal cameras can precisely distinguish moving objects such as people, animals, vehicles, leaves, raindrops or even shadows. A high level of functionality is guaranteed even in poor lighting conditions, such as darkness or fog.

Thermal cameras can also achieve a “synergy effect” in their designated task area with the help of AI. It works like this: the technology first collects raw data, which enables the system to learn and react independently to defined deviations in the production process. The field of application extends to quality control on the production line. For example, in metal foundries, the camera can immediately detect deviations from the thermal pattern when pressing in moulds. Continuous quality assurance minimises scrap and therefore reduces costs.

The more automated a process is, the more it must be monitored continuously. Due to its installation at neuralgic points, a thermal detection system can monitor a defined area of automation and initiate preventive measures. It can therefore be integrated into the entire production process to achieve a fully-automatic monitoring chain.

Measures to improve preventative fire protection are always welcome from an insurer’s point of view. The technical inspection centre VdS now certifies thermal detection systems so the technology can be implemented in existing, certified fire protection protocols. In combination with AI, various synergy effects can be achieved. In this respect, it will be interesting to observe whether these effects will also have an impact on established industry indicators.

Special thanks to Enno Hübers from Comp-Pro for the extensive information on application areas and technology.

Deutsche Rückversicherung

Aktiengesellschaft

Hansaallee 177

40549 Düsseldorf, Germany

Phone +49 211 4554-01

info@deutscherueck.de

www.deutscherueck.de

www.deutscherueck.com

www.drswiss.ch

Jan Stepic, Melanie Dahms, Stephanie Embach-Stein, Sven Klein

Andreas Meinhardt (responsible for contents)

intellitext SprachenService

www.intellitext.de

bernauer designbüro

www.bernauer-design.de

ENORM Digital GmbH

www.enorm.digital

Quang Ngoc Nguyen / Alamy Stock Photo

nattanai chimjanon / Alamy Stock Photo

Jack Malipan Travel Photography / Alamy Stock Photo

Azat Valeev / Shutterstock.com

Marccophoto / istockphoto.com

Published in December 2022

Sie verwenden einen veralteten Browser, in dem diese Seite möglicherweise nicht korrekt dargestellt wird.