Digitalisation has been a major driver of change in the insurance industry – and artificial intelligence has the potential to bring about further transformation. Decision-makers in the industry are aware of this, but many are still hesitant about implementing innovative technologies.

Insurers must use artificial intelligence (AI) if they want to remain competitive and AI-related investments belong at the top of the agenda. These are the findings of a study by IT service provider Adesso, which surveyed the general mood among decision-makers in the insurance industry. The study looked at the AI status quo – in terms of plans, projects and applications. “This is something I am convinced of: thanks to artificial intelligence, the insurance industry can position itself as one of the key players in the digital transformation,” says Stefan Riedel, an Adesso executive board member.

The huge application potential of AI is already emerging in the insurance industry. AI algorithms can analyse and process large amounts of data. The greater quantity of high-quality data available, the more precise their analyses will be and the more they can contribute to the creation of added value. Daily incoming data and a large inventory database make insurers ideal candidates to benefit from AI technologies, Riedel points out: “Whether for industrial plants, homes, health, mobility or retirement provisions, insurance companies have data from almost every aspect of life.”

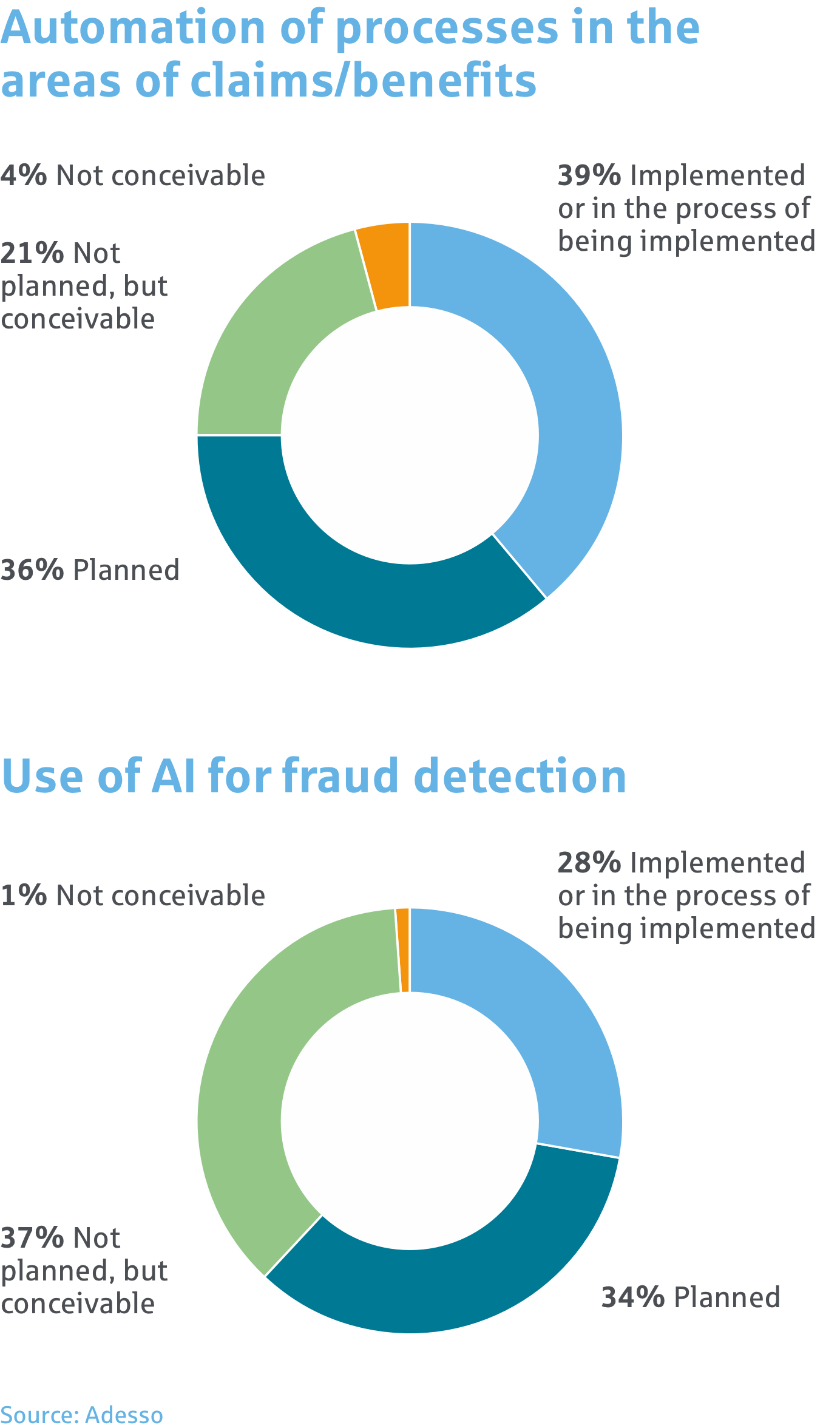

Three quarters of the insurance industry’s decision-makers surveyed in the Adesso study are already automating their workflows or are at least planning to address the issue. With the help of artificial intelligence, for example, they want to make claims management faster, cheaper and more efficient. Currently, claims handlers often still have to manually check submitted invoices from customers. AI-supported so-called “dark processing” (processing without human intervention) speeds up these procedures considerably. “AI could, for example, automatically analyse invoices and extract the most important items,” explains Ruben Wienigk, a data scientist at Deutsche Rück. It recognises the amount to be paid, the recipient and the recipient’s billing address – and all without human intervention. Customers would benefit from rapid processing and insurers from lower costs.

Every year, insurers in Germany suffer around five billion euros in losses due to fraud, according to the German Insurance Association (GDV). Artificial intelligence can help mitigate this problem, for example, by analysing digitally submitted documents or images of damages. AI-supported image forensics can be used to check whether an image has been digitally post-processed. A data comparison procedure exposes systematic fraudsters. To do this, the software scans the database and determines, almost in real time, whether an image has already served as evidence for previous claims. Fraud not only entails high costs for insurers but also a lot of work. Each suspected case must be subjected to an elaborate case-by-case examination. Artificial intelligence can identify discrepancies and make the claims adjuster’s job much easier.

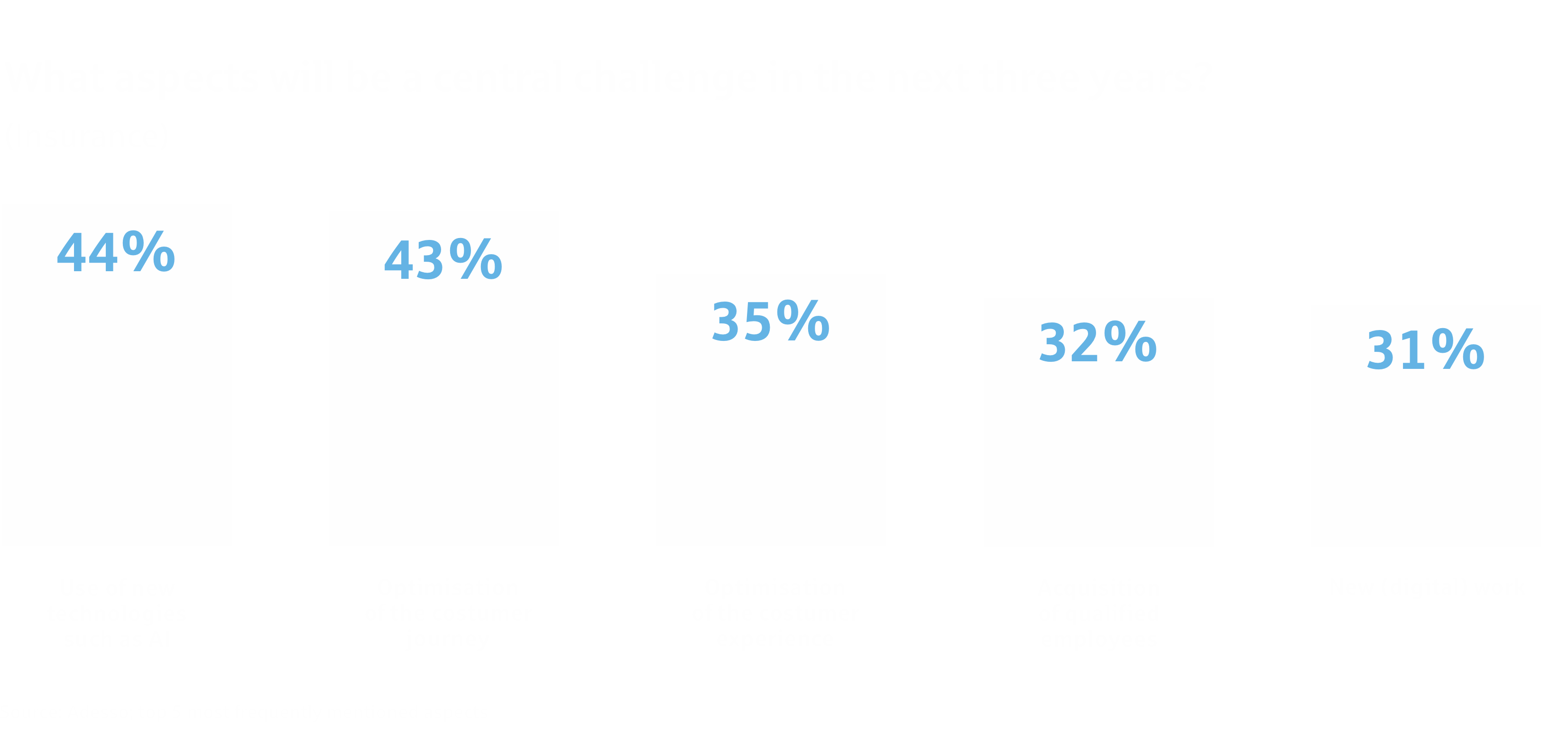

The results of the Adesso study show that the use of AI in the insurance industry is not yet widespread. More than 70% of respondents rate the industry’s position when it comes to AI as mediocre at best. Many insurers recognise the opportunities presented by the new technology but are slow to apply it. The reasons vary but in most cases, there is simply a lack of expertise, or companies are just not setting the right priorities. “You have to think AI projects through to the end, and the actual AI model represents only a small part of that,” says Wienigk. If, for example, AI is not embedded in productive IT systems, it cannot add any value and remains merely an experimental playground. Nevertheless, the Deutsche Rück data specialist is confident of one thing: “As experience grows, using AI will become much easier for insurers in the future.”

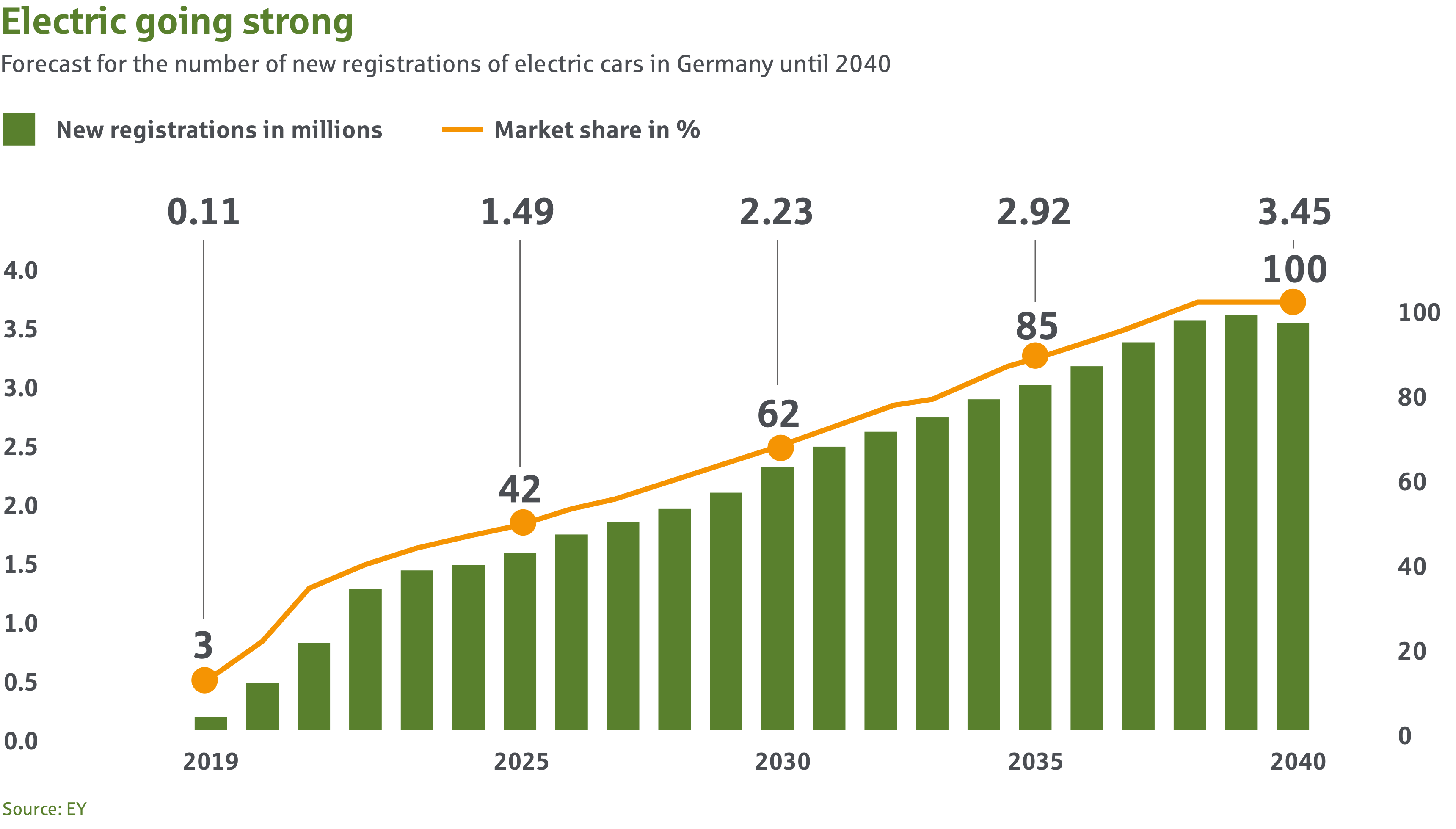

As growing numbers of people switch to electric vehicles with the help of government subsidies, insurers are now facing the challenge of adapting their products for this rapidly growing market.

Just a few years ago, a Tesla was an eye-catcher on Europe’s roads – now they are a common sighting on city streets. And the world market leader is not the only brand breaking sales records in many countries. Germany, for example, Europe’s largest economy, is now the world’s second largest market for electric vehicles. Despite the fact electric cars are still more expensive than comparable combustion vehicles, drivers are waking up to the benefits of premiums and tax incentives. And the trend towards higher fuel prices is making the case for electric increasingly compelling.

Rapid market changes and the special features of electric cars still pose challenges for motor insurers – both in terms of premiums and claims. In principle, the same rules apply to electric as to combustion engines – at least in Germany. The insurance premium here is calculated based on regional classification, mileage and a specific type of grading based on the model of car. Jörg Asmussen, chief executive of the German Insurance Association (GDV) explains: “If a car model causes comparatively few claims and low insurance payments on average, it receives a low-type class; if it causes many claims and high insurance payments, it receives a high-type class”. Due to high repair costs and expensive spare parts, electric cars belong in the higher type classes. This is because, according to GDV figures, the “claims requirements” for electric cars were almost 50 percent higher than for internal combustion vehicles in the period from 2017 to 2019.

But instead of adding the premium surcharge upfront, many insurers are luring electric car owners in with discounts on the premiums they need to pay – to appeal to new customer segments perhaps and to boost their sustainability credentials. Larissa Klick, a motor insurance business manager at Deutsche Rück, thinks it’s a risky policy. “Insurers sometimes offer premium discounts of up to 20% for electric cars and plug-in hybrids, artificially lowering the insurance premium for electric vehicles,” she says. As a result, many premiums are not risk-adequate. As long as the number of electric car owners among the insured is small, insurance companies can cope. However, as the number of electric vehicles increases, so does the financial risk to insurers if premiums do not cover the risk.

The consequences can already be seen in Norway, where new registrations of electric cars now exceed those of combustion-engine cars. Starting in 2025, the country plans to ban the sale of petrol and diesel vehicles. The rapid switch to electromobility is already impacting damages in comprehensive motor insurance which have become more expensive on average. The Norwegian claims ratio between 2015 to 2018 illustrates the growing pressure on comprehensive motor insurance: during this period, the ratio of claims expenses to premiums collected increased from 64% to around 78%. In response to increasing claims costs and the growth of electric car cover, motor insurance premiums increased by an average of 5% between 2018 and 2020. Premiums in other European countries could follow suit in the coming years.

In terms of the frequency of accidents and thefts, the GDV figures reveal no major differences between electric cars and conventionally powered vehicles in Germany. Nevertheless, repairing electric vehicles is often more expensive than repairing combustion-engine vehicles. This is not only because the parts are dearer, but also because the hourly rates of mechanics are higher – as many repairs can only be carried out by specialist mechanics. Moving forward, this means insurance salespeople must be able to provide a convincing explanation to customers questioning why electric car policies are more expensive.

But even if insurers manage to win over consumers to risk-adequate premiums, they will still face a great deal of uncertainty in the years to come – simply because the calculation of adequate premiums must be based on reliable data. But this is only available to a limited extent, and the situation will only slowly improve as electric cars become more widespread. In effect, insurers will have to live with a level of uncertainty in the short term – calculating their premiums for electric vehicles based on much less extensive data than for internal combustion vehicles – including the additional risk of any special premium discounts granted.

“In about five years, we will have sufficient data on claims,” Deutsche Rück expert Klick maintains. “At that point, we will be about as far along in electric car regulation and risk calculation as we are for internal combustion vehicles. Regulation remains key issue here, because that is from where insurers gain important experience for a reliable risk assessment”.

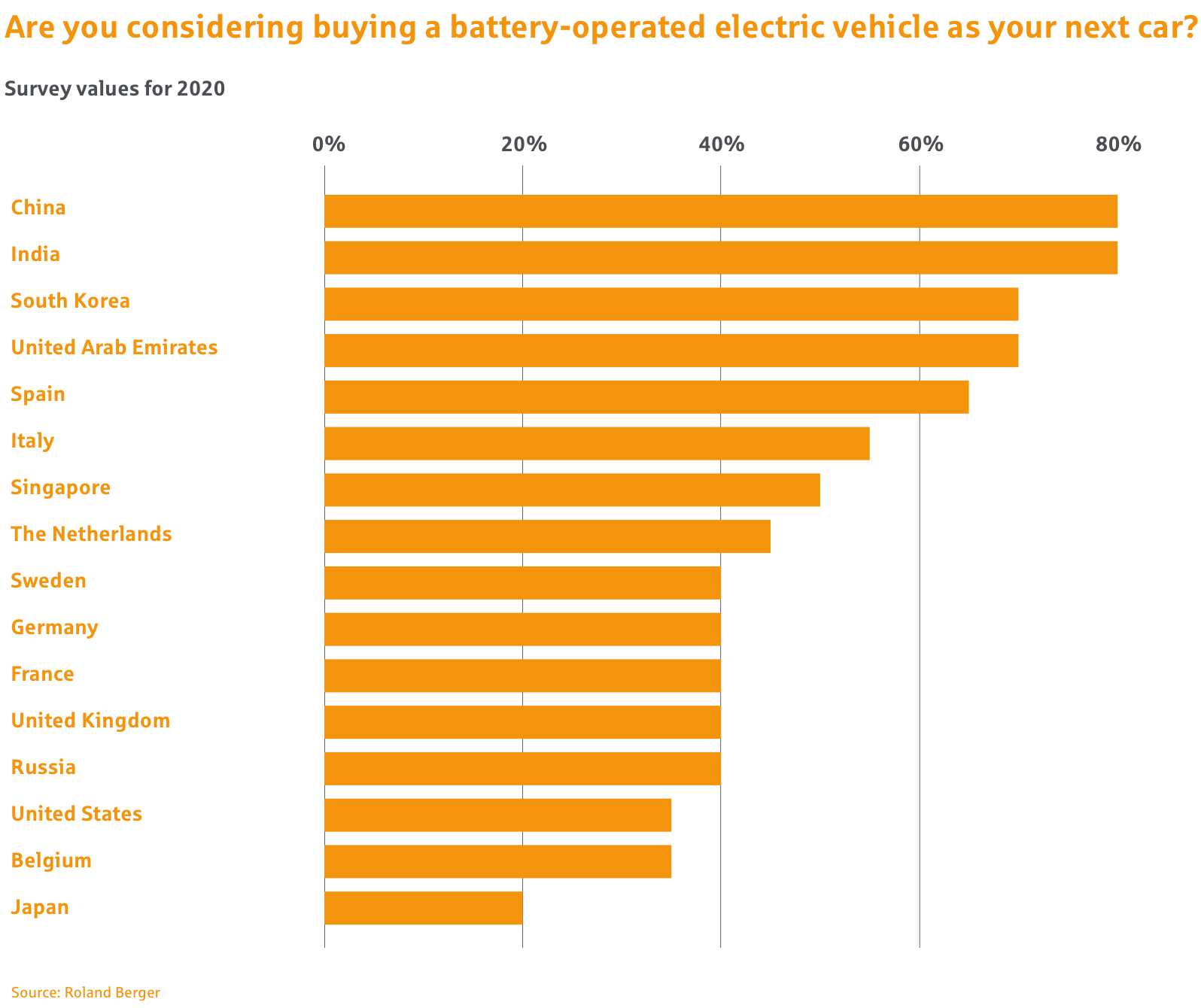

The swing towards e-mobility is gathering momentum around the world. However, there are striking differences in the speed of the transition globally: the top positions are taken primarily by countries that have government subsidy programs.

Hardly anyone outside of Asia has ever heard of the Hongguang Mini EV, the best-selling electric car in the first two months of 2021. In China, however, the model is already a familiar fixture in the transport landscape. Thanks to favourable registration regulations and tax benefits, the fully electric micro-SUV is available at a price electric car buyers in the West can only dream of. This is one of the reasons why more and more countries are following China’s lead in promoting electromobility with subsidies and purchase incentives.

The Paris Agreement made climate protection mandatory and a top priority for all 195 participating countries. The goal is for the European Union to become completely climate-neutral by 2050. To achieve this, there is no way around phasing out internal combustion engines and switching to e-mobility. The statistics look promising: even during the COVID-19 crisis, the number of electric cars worldwide continued to rise, surpassing the ten-million mark for the first time last year. In the first half of 2021 alone, sales figures increased by another 168%.

On figures alone, China is the global leader: around five million electric cars and half of all electric vehicles globally, can be found on the roads of the Asian superpower. In the current year, the Chinese market recorded a new sales record for so-called “new energy vehicles”, a collective term for electric cars, hydrogen cars and plug-in hybrids; one-and-a-half million of these vehicles were sold in China in the first half of the year.

Government funding has been successful in generating substantial demand. Buyers of environmentally friendly cars have long benefitted from tax breaks and purchase bonuses (which have only recently been reduced). However, in 2020, electric cars with a range of 400 kilometres or more were subsidised by the government with up to 3,000 euros. In addition, there were concerted efforts to bring affordable models to market as well. While acquisition costs were rising in Europe and the US, Chinese car manufacturers had electric cars in their line-up at eye-wateringly low prices around 3,700 euros.

The US lags behind China in the ranking of countries with the most electric vehicles. In fact, the number of new registrations of electric cars and plug-in hybrids has actually declined there in the past two years. In 2020, only 322,400 new electric vehicles were registered in the United States. China is also far ahead of the US in terms of technological innovation, despite Tesla’s Model 3 being the best-selling e-car in the world, with a total of over one million sold. The American president Joe Biden now wants to boost e-car sales countrywide with 174 billion dollars in purchase subsidies and premiums. The expansion of the charging infrastructure is also stipulated in the budget.

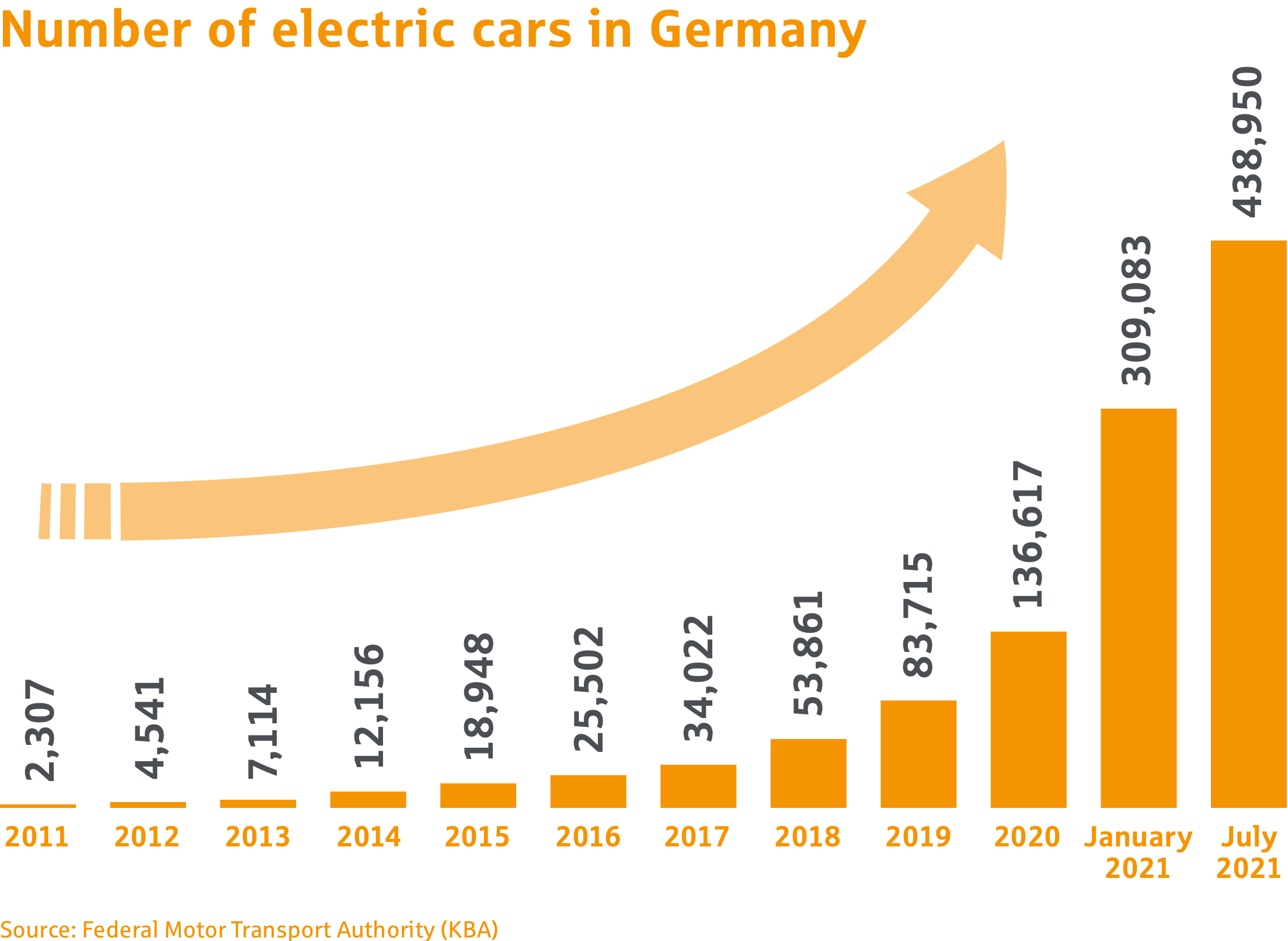

Although Germany has not yet caught up with the US in terms of electric car ownership, it has at least caught up in terms of new registrations. This ranks Germany as the world’s second-largest market for electromobility. Last year, almost 395,000 electric vehicles found new owners in Germany. One reason for these tremendous sales figures is government subsidies: buyers of a car with an electric drive receive a subsidy of up to 9,000 euros. In addition, converters are exempt from vehicle tax for ten years from the date of initial registration. To increase the density of the network of charging stations, the German government has earmarked investments of 300 million euros.

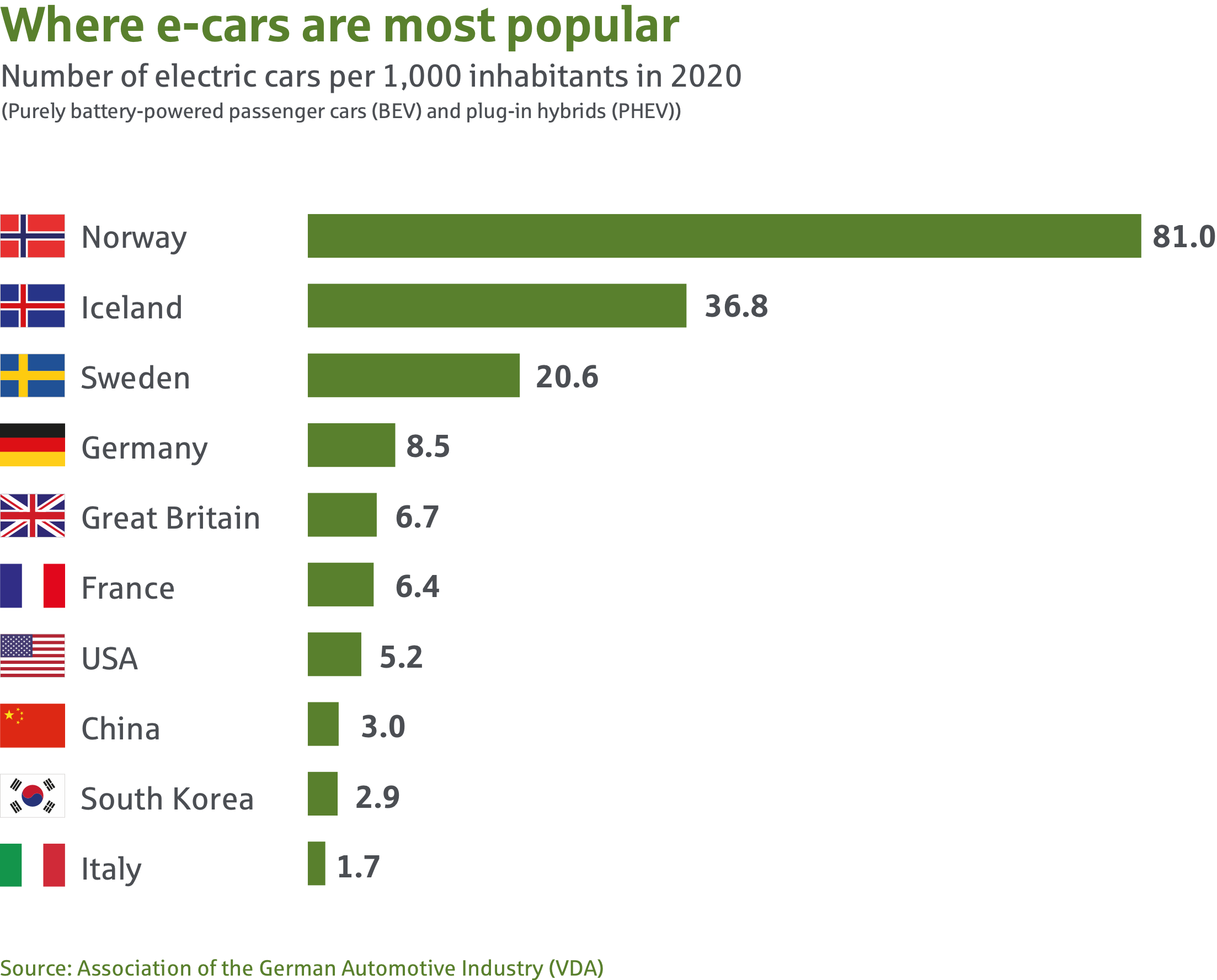

While it’s true that Germans have purchased more electric cars recently than people in other countries, in relation to the population, however, other nations are ahead. Nowhere in Europe are there more electric cars per capita than in Norway. Although the country is largely financed by oil exports, the proportion of cars with conventional drives is declining on its own roads and last year, electric alternatives accounted for more than half of all new cars sold.

As a climate pioneer, Norway created government incentives for electromobility at an early stage and set up support programs – the first as early as 1990. Today, electric cars are almost entirely exempt from vehicle tax. At the time of purchase, there is no registration tax, which is not the case for diesel and petrol vehicles. Other countries can learn a thing or two from the Scandinavian country when it comes to expanding the charging infrastructure. The Norwegians are well supplied with over 10,000 charging stations. This allows the government to set ambitious targets: by 2025, it plans to completely stop registering new internal combustion vehicles. Norway’s far-sighted policies serve as a model for other countries – in Europe and beyond.

Deutsche Rückversicherung

Aktiengesellschaft

Hansaallee 177

40549 Düsseldorf, Germany

Phone +49 211 4554-01

info@deutscherueck.de

www.deutscherueck.de

www.deutscherueck.com

www.drswiss.ch

Jan Stepic, Melanie Dahms, Stephanie Embach-Stein, Sven Klein

Andreas Meinhardt (responsible for contents)

intellitext SprachenService

www.intellitext.de

bernauer designbüro

www.bernauer-design.de

ENORM Digital GmbH

www.enorm.digital

shutterstock.com / temp-64GTX

shutterstock.com / PopTika

123rf.com / petovarga

Published in December 2021

Sie verwenden einen veralteten Browser, in dem diese Seite möglicherweise nicht korrekt dargestellt wird.